Summary

Gen Z is increasingly relying on “buy now, pay later” (BNPL) services for holiday shopping, with spending projected to rise 11.4% this year, totaling $18.5 billion.

These services appeal to younger consumers with limited credit histories but can lead to overextension, as they lack centralized reporting and encourage overspending.

Experts warn of accumulating fees, particularly when BNPL plans are tied to credit cards.

With inflation and rising credit card debt already burdening Gen Z, consumer advocates caution that these services may worsen financial instability despite their convenience.

It’s all well and good to blame the generation that can’t afford shit to use payday loan companies to buy shit…but when these companies align with the likes of Dominos Pizza to allow you to buy a pizza and pay off in several weekly installments, maybe it’s time to blame prices for being ridiculously high?

Pizza is not a necessity and adding predatory marketing doesn’t help. The whole point is to extract money from as many as possible including the ones that really cannot afford it.

Pizza is not a neccesity but at the end of the day we can’t expect everyone under 30 who doesn’t have well off parents to live on beans and rice. People aren’t robots and while no individual luxury is a neccesity, luxuries as a whole are a neccesity to some degree.

I’m going to be brutally honest.

- Corporations are shitstains and prey upon people’s minds and wants.

- People today are too entitled / greedy.

No. You don’t need that phone to survive, solid but low end one will easily carry you next 3-5 years. No, you do not need to go for McD for breakfast - eat a homemade sandwhich. Takes the same amount of time it’d take to get McD served to you.

But today a lot of folk take a lot of shit for granted or worse, needed, and it’s pitiful.

Fuck, that also is due to corporate ads and framing. But people need to wake up and stop fueling this shit on their own. And stop blaming schools - this shit is for parents to teach ffs, like the rest of actual household chores.

Also I am not arguing for everyone to live frugally but instead to learn a mindful way of spending. If you actually have free money, money you own and not a credit, then sure, treat yourself.

Systemic issues can only be solved with systemic changes…

No amount of shaming individuals will fix systemic debt issues, if this is such a large trend that it effects most of the generation then it can only be fixed with systemic changes.

The narrative that individuals are responsible for widespread debt is propaganda meant to shift blame off of the rich people causing wealth inequality to skyrocket

There is propaganda and then there is fact that nobody teaches their children about budgeting and financial responsibility. Do not treat credit like money you own, do not allow yourself to perceive luxury items as something you need, be mindful of what you can actually afford. Today people seem to have problems with these ideas - lack of education on the topic and aggressive ad campaigns by corporations resulted in that.

But while we cannot change masses, we not only can, but we should point this out to as many people as we can. Often all you need to notice something is for someone else to ask question about why that happens. And yeah, sure, maybe helping one or two people won’t make a dent, and even then these people may already be past saving or simply unable to pick up new habits. But if every mindful person tries to help someone else at least once, shift in society is guaranteed. And such shift will result, maybe, in actual change.

And, on a more flat approach - being aware of your own budgeting limits, spending power and how much money you use is not actually yours tends to radicalize people against the rich.

Only systemic changes can fix systemic issues .

This widespread propaganda needs to be countered with grassroots encouragement of more practical relationships with money though. That’s the cultural onus for systematic change. Don’t just shame them, but encourage everyone to live more responsibly and to vote for people who will reign in the creditors spreading this propaganda and loaning easy money to every financially irresponsible person

Without grassroots cultural change anyone who reigns this shit in will face political suicide for taking away their easy lines of credit. We see similar things with things like carbon taxation and other incentives to reduce carbon emissions that involve reducing overconsumption by all people (because yes, the average American is part of the problem too). The elites need to lose the most, but all of us need to live a financially and environmentally sustainable lifestyle and the systemic changes we all talk about wanting will impact our lives.

Only systemic changes will fix systemic issues

Oh wonderful and I suppose we should do nothing to bring those systemic changes about too? No systemic changes begin with changes to our community mindsets. The big creditors want you to not be talking about how they’re propagandizing to convince you to take easy lines of casual credit for fun little splurges and that that’s a trap and you shouldn’t take it. They want you to think that it’s not worth saving money and living within your means and they want you to keep up with the joneses and to make your friends uncomfortable not doing so. And most importantly they want people to feel like any expectation that they shouldn’t get instant and constant gratification is an unacceptable cost. When they get their way systemic change is infeasible. When they are seen as parasites lying to the masses and tricking them into living beyond their means, systemic change becomes possible. Politics are downstream of culture. You can’t change the policy neatly as easily as you can change the minds of those around you

Pretending like individual choices would do anything ignores the fact that these systemic issues can only be fixed with systemic changes

No amount of financial literacy will fix income inequality, we need to redistribute wealth if we want everyone to have the proportional wealth to participate in the economy.

It’s something I don’t understand. Writing this on a 5 year old phone that cost me 130 euros back then. I do have the money to buy any reasonable phone on the market (not some vanity ones for rich people to show off, but like the top of the line iPhone or Pixel, whatever).

But why would I when the old one still works and does everything I need? Why would I order food when I can just make something myself? If I want to treat myself, I go to a restaurant that I actually like and spend like 30 euros tops. That’s once every one or two months. Why do people overspend on this?

If you have kids and actually struggle with basic goods, that is something completely different. But I get the point you’re trying to make - some people just feel entitled to a standard of living that they can’t afford, and corporations gladly exploit that. And honestly, they’d be stupid not to. A sucker is born every minute. It’s up to the legislative to stop this predatory behavior because the market won’t regulate itself in this regard.

And you’re right, it’s not up to school to teach this - I wanted to comment on this one as well - school is supposed to turn you into a person that can think for yourself and realize that a high interest rate is something to your disadvantage. Not to exactly tell you what to do in situation X should you ever encounter it. Because society and its problems change and then suddenly what you learned no longer applies.

In the end, I can’t tell people how to spend their money. But once might make the case that with BNPL, people spend money that’s not not actually theirs yet. And once these people need help, is going to be society to foot bills, not the corporations who made money off it.

If your outlook on life is “work until you die with nothing left over”, might as well take back something first. The debt will pile up one way or another.

If were going to slip into a period of hyperinflation then taking on tons of consumer debt is just good financial planning.

Isn’t that only if wages increase alongside inflation

Oh no. If a fistfull of trillion dollar bills will buy you a shot glass of rice that maxed out credit card from the before time is pointless either way.

If $1,000 today is worth $5,000 tomorrow, you want to spend that $1,000 today so that when you pay up you only pay $1,000. Even if inflation hits you, you still only owe $1,000 no matter how much actual value those dollars still hold.

This is correct, although usually you’d want to go into debt on something like housing but let’s be honest, that’s not possible. Why not pay an 80 dollar door dash across four payments?

Why isn’t this framed as predatory lending?

I’m not sure because it definitely is.

The whole selling point of services like Klarna is they don’t show up on your credit checks, meaning you can very easily take on too much debt.

Because Capitalism demands exploitation

doesn’t mean we need to blame people (victims) rather than the organizations

Actually yes. Yes it does.

The poor are poor cuz they don’t work hard.

Can’t budget to help the homeless cuz some of them might trade food stamps for drugs.

If you didn’t want that baby you should have kept your lega closed.

Blaming the victim is as American as genociding the indigenous. Happens all day every day. Because this is the bad place.

After ending genocide at home it just exports it.

It’s not just American, it’s very British too.

Klarna is a Swedish company.

Ah, the great American Dream. Pull yourself up by your bootstraps and work hard to

enrich the millionaires profiting off your laborearn that $0.12 raise you’ve been asking for.

For the same reason that the subprime mortgage crisis wasn’t; line go up.

So, I’m going to come to their defence a bit here. Most of this is also covered in my comment I made further into the thread.

I don’t think previous generations were any less financially literate on average. You’ve always had those careful with credit and those that didn’t seem to care, or didn’t understand the ramifications of their decisions.

I grew up in the 80s and 90s and most large stores had their own store credit system with 30%+ APR rates. Plenty of people that were boomers or gen X had those accounts, and would routinely buy more whenever they cleared their credit a little.

You could also get credit cards and each card in terms of spending power would have similar limits to what you have now. And there was no shortage of people that would be sitting on their credit limit all the time. I knew people in the 90s that had no idea how interest worked and would be sitting on their credit limit paying back mostly interest all the time.

I think the difference is the ease with which you can gain access to credit now.

In the 80s and 90s you generally needed to go into the store to get their credit. You needed to go to a bank or fill in paperwork in the post to get credit cards. Crucially here, generally there were less providers of credit. Credit cards were often offered by banks, there were not so many resellers of credit. To gain a line of credit you had no chance to ever repay took more effort and as such wasn’t so much of a problem as it is now. It was still a problem, and companies routinely made money from the financially illiterate, even then.

What I think is different now, is that you can get credit from a few screen swipes on your phone now. There’s many many more providers of credit too. As such, the ability to get into an irreversible credit position is much easier. I would put money down that the same people with £1000s in various store credit/cards all compounding interest at 30%+ in the 90s, would also be in huge debt if credit were as easy to get then, as it is now.

I am going to blame financial institutions more here (those getting into the mess are not entirely free of blame). There might be over a thousand sources of credit now, but they all funnel up to a handful of large finance institutions, and they’re the ones really burying their head in the sand pretending they don’t know this is happening and couldn’t do anything to stop it. They most certainly could prevent it, if they wanted to. It just works better for them to have a generation that is constantly paying interest on never repayable debt. Even factoring in the few that will be written off.

Yes, ultimately we all have our own responsibility not to get into these situations. But I don’t think Gen Z or any generation are or were better at this on average. It’s just the conditions that allow it have changed, and continue to change.

they’re the ones really burying their head in the sand pretending they don’t know this is happening and couldn’t do anything to stop it.

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.”

You can actually survive without streaming services and online subscriptions.

Is this today’s avocado toast?

Man imagine the privilege of worrying about not having streaming services as an essential need.

It’s today’s variant of “beans and rice cost, x. So why are you complaining about food cost?”

deleted by creator

Who is teaching them financial literacy in the first place? Because they aren’t being taught it in schools. Meanwhile, these predatory companies do everything they can to convince people to use them.

Cool, except I was very clearly talking about the financial literacy to not do things like get suckered by a predatory lender.

Why are you against that?

This is the level of discourse at this point. Someone makes an observation or a comment and people think responding with a meme is a “gotcha.”

No wonder everything is fucked.

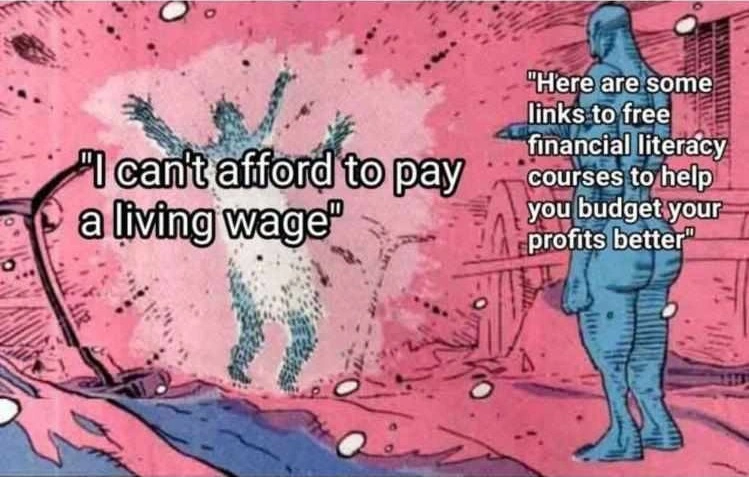

The label on the on the guy being explode talks about paying your staff a living wage. Basically, it’s a dunk on arguments that raising the minimum wage would loose jobs.

And it had absolutely nothing to do with what I was talking about besides the term “financial literacy.”

If you don’t think it’s sensible to teach young people to avoid predatory lenders before it’s too late, just say so. Otherwise this is irrelevant.

You cannot budget your way out of poverty. “Financial literacy” is just capitalists kicking the can down the road.

I think it is highly unlikely that all of the Gen Z people getting these loans came out of a life of poverty.

deleted by creator

It’s not, though. Financial literacy includes things like, not spending money you don’t have. When you take these predatory loans to get goods, you end up more enslaved to the capitalist system and to those who have money to lend.

Financial literacy is not a cure-all, just like normal literacy doesn’t make you understand Shakespeare.

And they call them predatory loans for a reason. They are coming to you and they are going to hurt you. But we don’t teach kids this before they get into the adult world and this is the result.

Coming soon: Predator Loans Vs Loan Sharks

In cinemas just as soon as we pay off our bills.

Yeah, and financial literacy alone may not get you out of poverty, and it definitely won’t get everyone out of poverty, but among those with the possibility of class mobility financial literacy will play a role in where they wind up.

If the outcome is the same whether you save up or not - you’ll never be able to afford anything - why now “own” things while you can?

Well when the world is about to end in multiple ways at once, why with about debt?

Keep on buying plastic shit, I’m sure it’s gonna be fucken great.

It’s almost like the “services” are designed just for this…

I hate BNPY so much… I deleted my after pay account, which means I can no long use their services unless I get in contact with support to reopen my account. I did it to explicitly make it near impossible for me to be tempted. It worked. There were times I felt regret, but it was 100% the smartest move.

Then, PayPal introduced pay in 4… All my hard work went right down the drain. I can’t afford this shit but fuck it’s hard when you’re clinically depressed.

Services should be required to allow you to opt out of being offered such things. I choose to live a debt minimal lifestyle because of how I was raised, and I don’t want to be tempted. The same goes for online gambling. (And alcohol advertisements, but I do drink).

Does it matter. It seems that a lot of them have checked out already as they see the world burning around them.

Hard to blame them.

BNPL is a credit card but in app.

Nah more credit check hits

No, bnpl do soft pull, so that credit check doesn’t hit your credit score (unless you default on bnpl)